VIX Futures Hit New Record Short: Is A Historic Volatility Squeeze Coming?

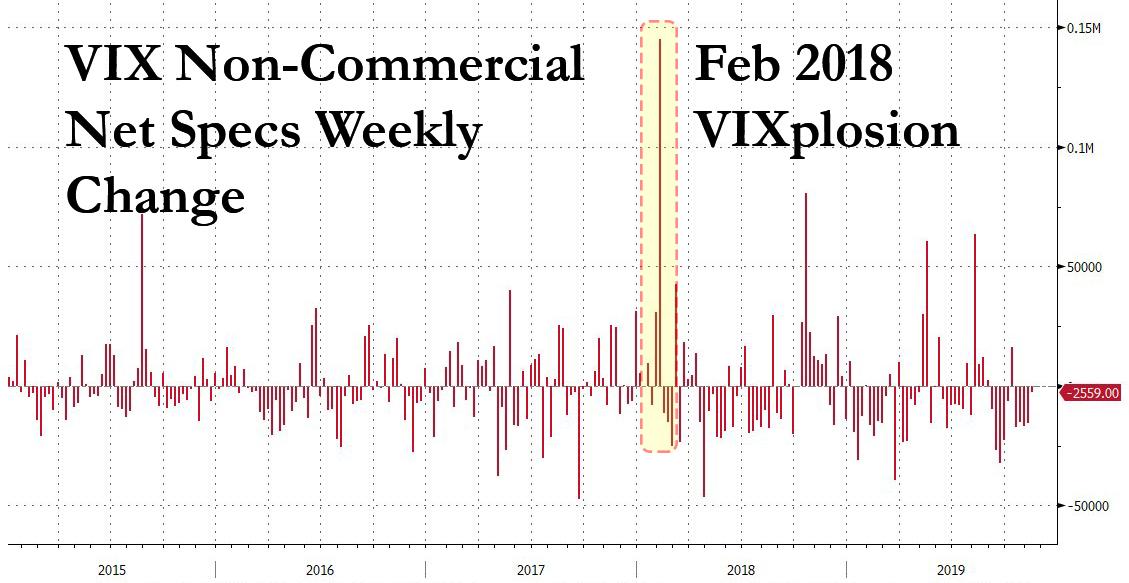

If Fishman is correct, there is never point in worrying about record VIX net spec exposure ever, as every position merely represents an offset to an equally matched long position somewhere else. We know that’s incorrect however, because the biggest one week surge on record in non-commercial specs took place during the February 2018 VIXplosion week, which confirms that not only were ETPs not perfectly hedged, but there was an epic VIX short squeeze which as many recall sent spot VIX into the 50s.

SO FOR ALL THOSE WHO HOPE TO MITIGATE THE IMPORTANCE OF A RECORD VIX NET SHORT IN FUTURES, NOT ONLY DO WE DISAGREE THAT THIS POSITION IS “PERFECTLY” HEDGE WITH COMMERCIAL LONGS, BUT SINCE NON-COMMERCIAL ACTORS ARE MORE LIKELY TO REVERSE POSITIONS, CATCHING COMMERCIAL LONGS OFFSIDE AND UNWILLING TO PART WITH THEIR LONGS, IT IS OUR BELIEF THAT THE POTENTIAL FOR A HISTORIC VIX SHORT SQUEEZE IS NOW FAR GREATER THAN IT WAS DURING THE FEB 2018 VIXPLOSION WHICH ENDED UP WIPING OUT ALL THOSE WHO WERE LONG INVERSE VIX ETNS. WE, FOR ONE, CAN’T WAIT TO FIND OUT JUST WHAT “COLLECTING PENNIES IN FRONT OF A STEAMROLLER” TRADE WILL BE WIPED OUT DURING THE NEXT EPIC VIX SQUEEZE.

ISEE INDEX

All Securities=100–UNCH

All Equities Only=140%

All Indexes & ETFs Only=82UNCH

ISEE Sentiment Index

Investors often buy call and put options to express their actual market view of a particular stock, and because of that, opening such long transactions are thought to best represent market sentiment. Market maker and firm trades, which are excluded, are not considered representative of true market sentiment due to their specialized nature. As such, the ISEE calculation method allows for a more accurate measure of true investor sentiment than traditional put/call ratios.

Because of this distinctive calculation methodology, ISEE has been referenced by The Wall Street Journal, Barron’s and other leading publications as a useful investment tool. Investors and investment professionals can use this unique put/call value to determine how other investors view stock prices, as well as to supplement and validate their own market views.